Short term macroeconomic dynamics

- The unequal effects of the health-economy tradeoff during the COVID-19 pandemic, 2023. Nature Human Behavior [Open Access]. Show More

The potential tradeoff between health outcomes and economic impact has been a major challenge in the policy making process during the COVID-19 pandemic. Epidemic-economic models designed to address this issue are either too aggregate to consider heterogeneous outcomes across socio-economic groups, or, when sufficiently fine-grained, not well grounded by empirical data. To fill this gap, we introduce a data-driven, granular, agent-based model that simulates epidemic and economic outcomes across industries, occupations, and income levels with geographic realism. The key mechanism coupling the epidemic and economic modules is the reduction in consumption demand due to fear of infection. We calibrate the model to the first wave of COVID-19 in the New York metropolitan area, showing that it reproduces key epidemic and economic statistics, and then examine counterfactual scenarios. We find that: (a) both high fear of infection and strict restrictions similarly harm the economy but reduce infections; (b) low-income workers bear the brunt of both the economic and epidemic harm; (c) closing non-customer-facing industries such as manufacturing and construction only marginally reduces the death toll while considerably increasing unemployment; and (d) delaying the start of protective measures does little to help the economy and worsens epidemic outcomes in all scenarios. We anticipate that our model will help designing effective and equitable non-pharmaceutical interventions that minimize disruptions in the face of a novel pandemic.

The potential tradeoff between health outcomes and economic impact has been a major challenge in the policy making process during the COVID-19 pandemic. Epidemic-economic models designed to address this issue are either too aggregate to consider heterogeneous outcomes across socio-economic groups, or, when sufficiently fine-grained, not well grounded by empirical data. To fill this gap, we introduce a data-driven, granular, agent-based model that simulates epidemic and economic outcomes across industries, occupations, and income levels with geographic realism. The key mechanism coupling the epidemic and economic modules is the reduction in consumption demand due to fear of infection. We calibrate the model to the first wave of COVID-19 in the New York metropolitan area, showing that it reproduces key epidemic and economic statistics, and then examine counterfactual scenarios. We find that: (a) both high fear of infection and strict restrictions similarly harm the economy but reduce infections; (b) low-income workers bear the brunt of both the economic and epidemic harm; (c) closing non-customer-facing industries such as manufacturing and construction only marginally reduces the death toll while considerably increasing unemployment; and (d) delaying the start of protective measures does little to help the economy and worsens epidemic outcomes in all scenarios. We anticipate that our model will help designing effective and equitable non-pharmaceutical interventions that minimize disruptions in the face of a novel pandemic.

- Forecasting the propagation of pandemic shocks with a dynamic input-output model, 2022. Journal of Economic Dynamics and Control [Open Access]. New version of: Production networks and epidemic spreading: How to restart the UK economy?, 2020. Covid Economics, Arxiv, Twitter summary, VoxEU Show More

We introduce a dynamic disequilibrium input-output model that was used to forecast the economics of the COVID-19 pandemic. This model was designed to understand the upstream and downstream propagation of the industry-specific demand and supply shocks caused by COVID-19, which were exceptional in their severity, suddenness and heterogeneity across industries. The model, which was inspired in part by previous work on the response to natural disasters, includes the introduction of a new functional form for production functions, which allowed us to create bespoke production functions for each industry based on a survey of industry analysts. We also introduced new elements for modeling inventories, consumption and labor. The resulting model made accurate real-time forecasts for the decline of sectoral and aggregate economic activity in the United Kingdom in the second quarter of 2020. We examine some of the theoretical implications of our model and find that the choice of production functions and inventory levels plays a key role in the propagation of pandemic shocks. Our work demonstrates that an out of equilibrium model calibrated against national accounting data can serve as a useful real time policy evaluation and forecasting tool.

- Synchronization of endogenous business cycles, 2023. Arxiv, SSRN, LEM Working Paper Show More

Business cycles tend to comove across countries. However, standard models that attribute comovement to propagation of exogenous shocks struggle to generate a level of comovement that is as high as in the data. In this paper, we consider models that produce business cycles endogenously, through some form of non-linear dynamics — limit cycles or chaos. These models generate stronger comovement, because they combine shock propagation with synchronization of endogenous dynamics. In particular, we study a demand-driven model in which business cycles emerge from strategic complementarities within countries, synchronizing their oscillations through international trade linkages. We develop an eigendecomposition that explores the interplay between non-linear dynamics, shock propagation and network structure, and use this theory to understand the mechanisms of synchronization. Next, we calibrate the model to data on 24 countries and show that the empirical level of comovement can only be matched by combining endogenous business cycles with exogenous shocks. Our results lend support to the hypothesis that business cycles are at least in part caused by underlying non-linear dynamics.

Business cycles tend to comove across countries. However, standard models that attribute comovement to propagation of exogenous shocks struggle to generate a level of comovement that is as high as in the data. In this paper, we consider models that produce business cycles endogenously, through some form of non-linear dynamics — limit cycles or chaos. These models generate stronger comovement, because they combine shock propagation with synchronization of endogenous dynamics. In particular, we study a demand-driven model in which business cycles emerge from strategic complementarities within countries, synchronizing their oscillations through international trade linkages. We develop an eigendecomposition that explores the interplay between non-linear dynamics, shock propagation and network structure, and use this theory to understand the mechanisms of synchronization. Next, we calibrate the model to data on 24 countries and show that the empirical level of comovement can only be matched by combining endogenous business cycles with exogenous shocks. Our results lend support to the hypothesis that business cycles are at least in part caused by underlying non-linear dynamics.

Theory of Agent-Based Models

- On learning agent-based models from data, with C. Monti, G. De Francisci Morales, F. Bonchi, 2023. Scientific Reports [Open Access]. Show More

Agent-Based Models (ABMs) are used in several fields to study the evolution of complex systems from micro-level assumptions. However, ABMs typically can not estimate agent-specific (or “micro”) variables: this is a major limitation which prevents ABMs from harnessing micro-level data availability and which greatly limits their predictive power. In this paper, we propose a protocol to learn the latent micro-variables of an ABM from data. The first step of our protocol is to reduce an ABM to a probabilistic model, characterized by a computationally tractable likelihood. This reduction follows two general design principles: balance of stochasticity and data availability, and replacement of unobservable discrete choices with differentiable approximations. Then, our protocol proceeds by maximizing the likelihood of the latent variables via a gradient-based expectation maximization algorithm. We demonstrate our protocol by applying it to an ABM of the housing market, in which agents with different incomes bid higher prices to live in high-income neighborhoods. We demonstrate that the obtained model allows accurate estimates of the latent variables, while preserving the general behavior of the ABM. We also show that our estimates can be used for out-of-sample forecasting. Our protocol can be seen as an alternative to black-box data assimilation methods, that forces the modeler to lay bare the assumptions of the model, to think about the inferential process, and to spot potential identification problems.

Agent-Based Models (ABMs) are used in several fields to study the evolution of complex systems from micro-level assumptions. However, ABMs typically can not estimate agent-specific (or “micro”) variables: this is a major limitation which prevents ABMs from harnessing micro-level data availability and which greatly limits their predictive power. In this paper, we propose a protocol to learn the latent micro-variables of an ABM from data. The first step of our protocol is to reduce an ABM to a probabilistic model, characterized by a computationally tractable likelihood. This reduction follows two general design principles: balance of stochasticity and data availability, and replacement of unobservable discrete choices with differentiable approximations. Then, our protocol proceeds by maximizing the likelihood of the latent variables via a gradient-based expectation maximization algorithm. We demonstrate our protocol by applying it to an ABM of the housing market, in which agents with different incomes bid higher prices to live in high-income neighborhoods. We demonstrate that the obtained model allows accurate estimates of the latent variables, while preserving the general behavior of the ABM. We also show that our estimates can be used for out-of-sample forecasting. Our protocol can be seen as an alternative to black-box data assimilation methods, that forces the modeler to lay bare the assumptions of the model, to think about the inferential process, and to spot potential identification problems. - Sensitivity analysis of agent-based models: a new protocol, with E. Borgonovo, J. Rivkin, L. Rizzo, N. Siggelkow, 2022. Computational and Mathematical Organization Theory [Open Access], Twitter summary Show More

Agent-based models (ABMs) are increasingly used in the management sciences. Though useful, ABMs are often critiqued: it is hard to discern why they produce the results they do and whether other assumptions would yield similar results. To help researchers address such critiques, we propose a systematic approach to conducting sensitivity analyses of ABMs. Our approach deals with a feature that can complicate sensitivity analyses: most ABMs include important non-parametric elements, while most sensitivity analysis methods are designed for parametric elements only. The approach moves from charting out the elements of an ABM through identifying the goal of the sensitivity analysis to specifying a method for the analysis. We focus on four common goals of sensitivity analysis: determining whether results are robust, which elements have the greatest impact on outcomes, how elements interact to shape outcomes, and which direction outcomes move when elements change. For the first three goals, we suggest a combination of randomized finite change indices calculation through a factorial design. For direction of change, we propose a modification of individual conditional expectation (ICE) plots to account for the stochastic nature of the ABM response. We illustrate our approach using the Garbage Can Model, a classic ABM that examines how organizations make decisions.

Convergence of learning in games

- Towards a taxonomy of learning dynamics in 2×2 games, with J. B. T. Sanders, T. Galla and J. D. Farmer, 2022. Games and Economic Behavior, Arxiv, SSRN, Twitter summary Show More

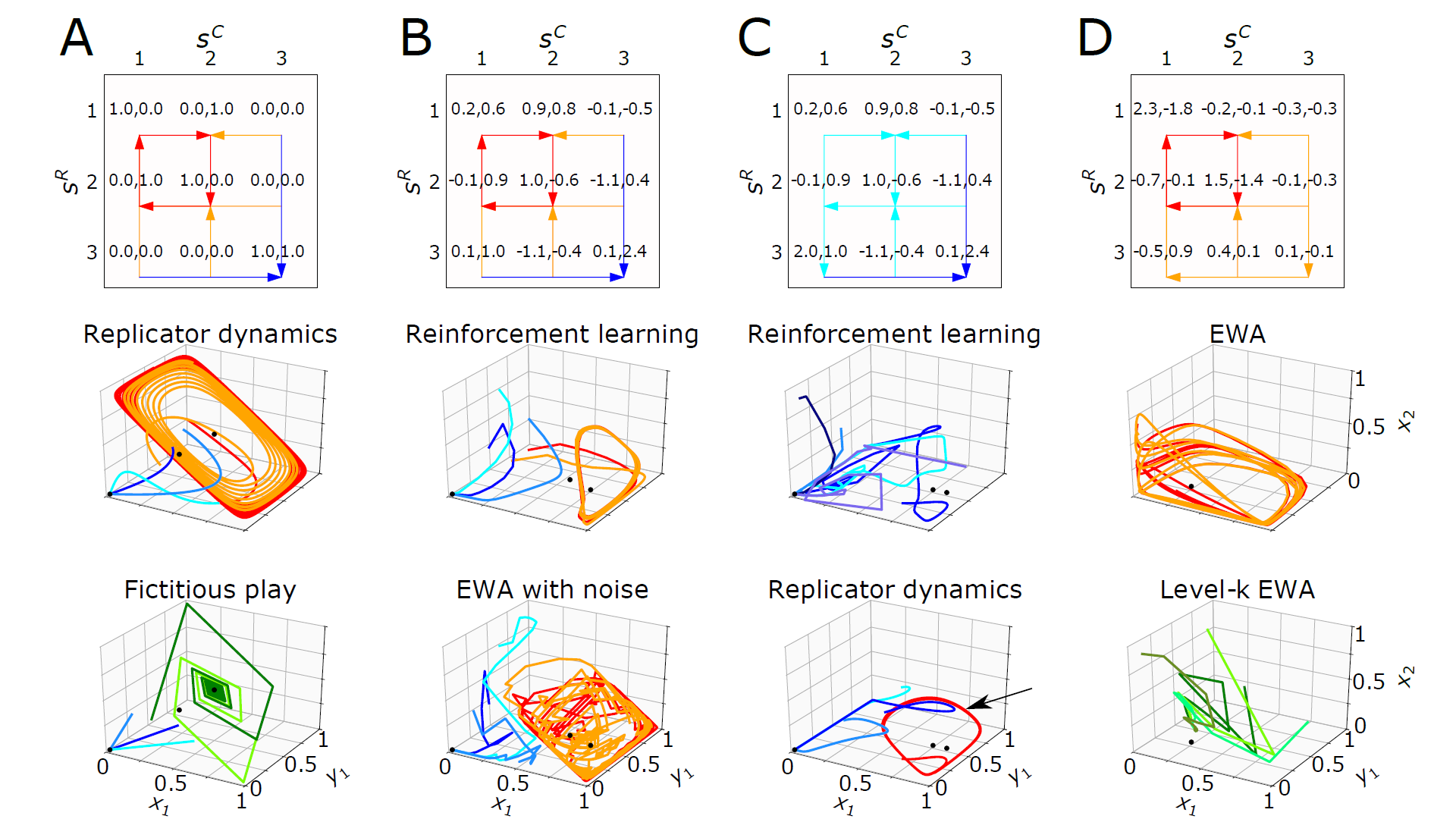

Do boundedly rational players learn to choose equilibrium strategies as they play a game repeatedly? A large literature in behavioral game theory has proposed and experimentally tested various learning algorithms, but a comparative analysis of their equilibrium convergence properties is lacking. In this paper we analyze Experience-Weighted Attraction (EWA), which generalizes fictitious play, best-response dynamics, reinforcement learning and also replicator dynamics. Studying 2×2 games for tractability, we recover some well-known results in the limiting cases in which EWA reduces to the learning rules that it generalizes, but also obtain new results for other parameterizations. For example, we show that in coordination games EWA may only converge to the Pareto-efficient equilibrium, never reaching the Pareto-inefficient one; that in Prisoner Dilemma games it may converge to fixed points of mutual cooperation; and that limit cycles or chaotic dynamics may be more likely with longer or shorter memory of previous play.

Do boundedly rational players learn to choose equilibrium strategies as they play a game repeatedly? A large literature in behavioral game theory has proposed and experimentally tested various learning algorithms, but a comparative analysis of their equilibrium convergence properties is lacking. In this paper we analyze Experience-Weighted Attraction (EWA), which generalizes fictitious play, best-response dynamics, reinforcement learning and also replicator dynamics. Studying 2×2 games for tractability, we recover some well-known results in the limiting cases in which EWA reduces to the learning rules that it generalizes, but also obtain new results for other parameterizations. For example, we show that in coordination games EWA may only converge to the Pareto-efficient equilibrium, never reaching the Pareto-inefficient one; that in Prisoner Dilemma games it may converge to fixed points of mutual cooperation; and that limit cycles or chaotic dynamics may be more likely with longer or shorter memory of previous play. - Best-response dynamics, playing sequences, and convergence to equilibrium in random games, with Torsten Heinrich, Yoojin Jang, Luca Mungo, Alex Scott, Bassel Tarbush, Samuel Wiese, 2023. International Journal of Game Theory [Open Access]. Show More

We show that the playing sequence–the order in which players update their actions–is a crucial determinant of whether the best-response dynamic converges to a Nash equilibrium. Specifically, we analyze the probability that the best-response dynamic converges to a pure Nash equilibrium in random n-player m-action games under three distinct playing sequences: clockwork sequences (players take turns according to a fixed cyclic order), random sequences, and simultaneous updating by all players. We analytically characterize the convergence properties of the clockwork sequence best-response dynamic. Our key asymptotic result is that this dynamic almost never converges to a pure Nash equilibrium when $n$ and $m$ are large. By contrast, the random sequence best-response dynamic converges almost always to a pure Nash equilibrium when one exists and n and m are large. The clockwork best-response dynamic deserves particular attention: we show through simulation that, compared to random or simultaneous updating, its convergence properties are closest to those exhibited by three popular learning rules that have been calibrated to human game-playing in experiments (reinforcement learning, fictitious play, and replicator dynamics).

We show that the playing sequence–the order in which players update their actions–is a crucial determinant of whether the best-response dynamic converges to a Nash equilibrium. Specifically, we analyze the probability that the best-response dynamic converges to a pure Nash equilibrium in random n-player m-action games under three distinct playing sequences: clockwork sequences (players take turns according to a fixed cyclic order), random sequences, and simultaneous updating by all players. We analytically characterize the convergence properties of the clockwork sequence best-response dynamic. Our key asymptotic result is that this dynamic almost never converges to a pure Nash equilibrium when $n$ and $m$ are large. By contrast, the random sequence best-response dynamic converges almost always to a pure Nash equilibrium when one exists and n and m are large. The clockwork best-response dynamic deserves particular attention: we show through simulation that, compared to random or simultaneous updating, its convergence properties are closest to those exhibited by three popular learning rules that have been calibrated to human game-playing in experiments (reinforcement learning, fictitious play, and replicator dynamics). - Best reply structure and equilibrium convergence in generic games, with T. Heinrich and J. D. Farmer, 2019. Science Advances [Open Access] Show More

Game theory is widely used to model interacting biological and social systems. In some situations, players may converge to an equilibrium, e.g., a Nash equilibrium, but in other situations their strategic dynamics oscillate endogenously. If the system is not designed to encourage convergence, which of these two behaviors can we expect a priori? To address this question, we follow an approach that is popular in theoretical ecology to study the stability of ecosystems: We generate payoff matrices at random, subject to constraints that may represent properties of real-world games. We show that best reply cycles, basic topological structures in games, predict nonconvergence of six well-known learning algorithms that are used in biology or have support from experiments with human players. Best reply cycles are dominant in complicated and competitive games, indicating that in this case equilibrium is typically an unrealistic assumption, and one must explicitly model the dynamics of learning.

Game theory is widely used to model interacting biological and social systems. In some situations, players may converge to an equilibrium, e.g., a Nash equilibrium, but in other situations their strategic dynamics oscillate endogenously. If the system is not designed to encourage convergence, which of these two behaviors can we expect a priori? To address this question, we follow an approach that is popular in theoretical ecology to study the stability of ecosystems: We generate payoff matrices at random, subject to constraints that may represent properties of real-world games. We show that best reply cycles, basic topological structures in games, predict nonconvergence of six well-known learning algorithms that are used in biology or have support from experiments with human players. Best reply cycles are dominant in complicated and competitive games, indicating that in this case equilibrium is typically an unrealistic assumption, and one must explicitly model the dynamics of learning.

Housing markets

- What do online listings tell us about the housing market?, with M. Loberto and A. Luciani, 2022. International Journal of Central Banking [Open Access] Show More

Since the Great Recession, central banks and macroprudential authorities have been devoting much more attention to the housing market. To properly assess trends and risks, policymakers need detailed, timely, and granular information on demand, supply, and transactions. This information is hardly provided by traditional survey or administrative data. In this paper, we argue that data coming from housing sales advertisements (ads) websites can be used to overcome some existing deficiencies. Using a large data set of ads in Italy, we provide the first comprehensive analysis of the problems and potential of these data. We show how machine learning tools can correct a specific bias of online listings, namely the proliferation of duplicate ads that refer to the same housing unit, increasing the representativeness and reliability of these data. We then show how the timeliness, granularity, and online nature of these data make it possible to monitor in real-time housing demand, supply, and prices.

Since the Great Recession, central banks and macroprudential authorities have been devoting much more attention to the housing market. To properly assess trends and risks, policymakers need detailed, timely, and granular information on demand, supply, and transactions. This information is hardly provided by traditional survey or administrative data. In this paper, we argue that data coming from housing sales advertisements (ads) websites can be used to overcome some existing deficiencies. Using a large data set of ads in Italy, we provide the first comprehensive analysis of the problems and potential of these data. We show how machine learning tools can correct a specific bias of online listings, namely the proliferation of duplicate ads that refer to the same housing unit, increasing the representativeness and reliability of these data. We then show how the timeliness, granularity, and online nature of these data make it possible to monitor in real-time housing demand, supply, and prices. - Home is where the ad is: online interest proxies housing demand, with M. Loberto, 2018. EPJ Data Science [Open Access], Twitter summary Show More

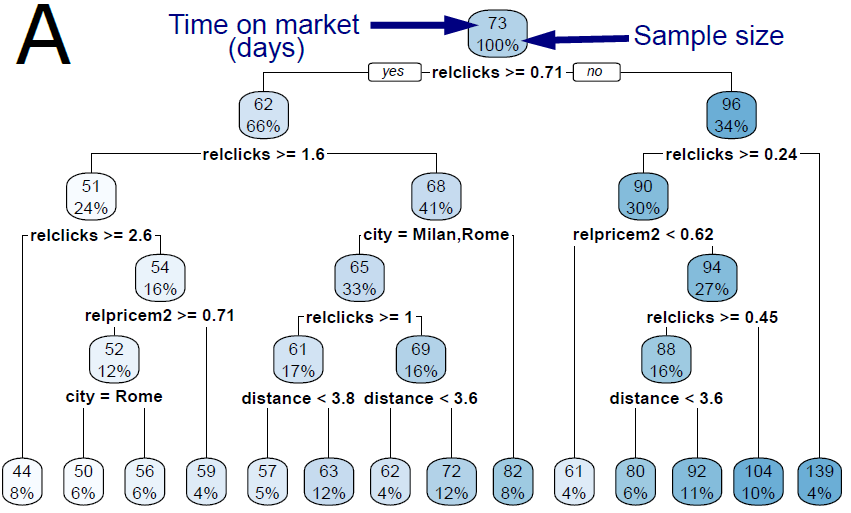

Online activity leaves digital traces of human behavior. In this paper we investigate if online interest can be used as a proxy of housing demand, a key yet so far mostly unobserved feature of housing markets. We analyze data from an Italian website of housing sales advertisements (ads). For each ad, we know the timings at which website users clicked on the ad or used the corresponding contact form. We show that low online interest—a small number of clicks/contacts on the ad relative to other ads in the same neighborhood—predicts longer time on market and higher chance of downward price revisions, and that aggregate online interest is a leading indicator of housing market liquidity and prices. As online interest affects time on market, liquidity and prices in the same way as actual demand, we deduce that it is a good proxy. We then turn to a standard econometric problem: what difference in demand is caused by a difference in price? We use machine learning to identify pairs of duplicate ads, i.e. ads that refer to the same housing unit. Under some caveats, differences in demand between the two ads can only be caused by differences in price. We find that a 1% higher price causes a 0.66% lower number of clicks.

Online activity leaves digital traces of human behavior. In this paper we investigate if online interest can be used as a proxy of housing demand, a key yet so far mostly unobserved feature of housing markets. We analyze data from an Italian website of housing sales advertisements (ads). For each ad, we know the timings at which website users clicked on the ad or used the corresponding contact form. We show that low online interest—a small number of clicks/contacts on the ad relative to other ads in the same neighborhood—predicts longer time on market and higher chance of downward price revisions, and that aggregate online interest is a leading indicator of housing market liquidity and prices. As online interest affects time on market, liquidity and prices in the same way as actual demand, we deduce that it is a good proxy. We then turn to a standard econometric problem: what difference in demand is caused by a difference in price? We use machine learning to identify pairs of duplicate ads, i.e. ads that refer to the same housing unit. Under some caveats, differences in demand between the two ads can only be caused by differences in price. We find that a 1% higher price causes a 0.66% lower number of clicks.

- Residential Income Segregation: A Behavioral Model of the Housing Market, with J.P. Nadal and A. Vignes, 2019. Journal of Economic Behavior and Organization, Arxiv, SSRN Show More

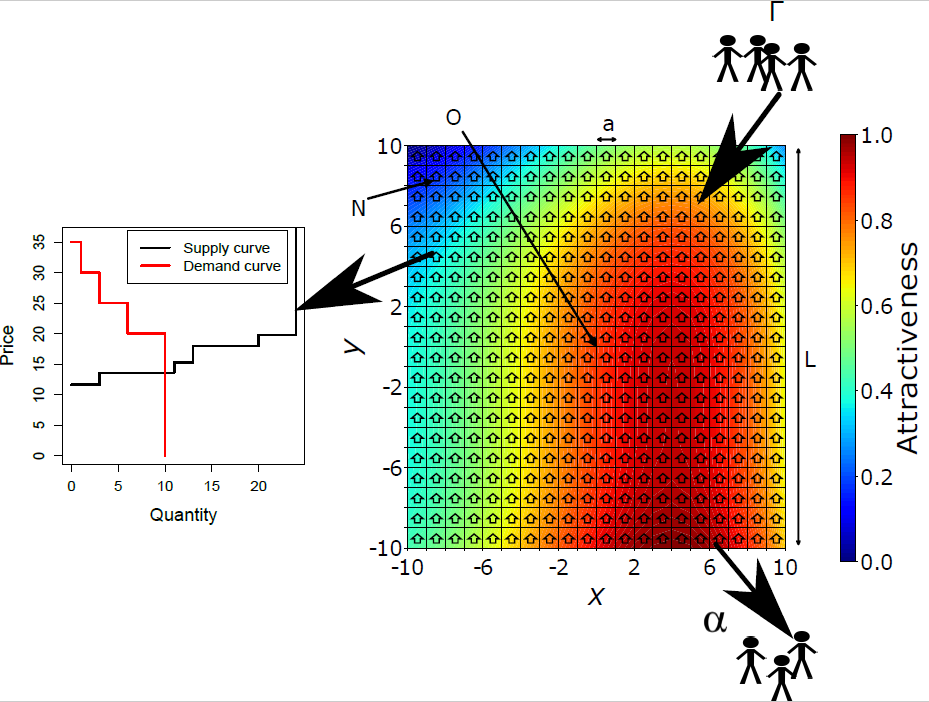

We represent the functioning of the housing market and study the relation between income segregation, income inequality and house prices by introducing a spatial Agent-Based Model (ABM). Differently from traditional models in urban economics, we explicitly specify the behavior of buyers and sellers and the price formation mechanism. Buyers who differ by income select among heterogeneous neighborhoods using a probabilistic model of residential choice; sellers employ an aspiration level heuristic to set their reservation offer price; prices are determined through a continuous double auction. We first provide an approximate analytical solution of the ABM, shedding light on the structure of the model and on the effect of the parameters. We then simulate the ABM and find that: (i) a more unequal income distribution lowers the prices globally, but implies stronger segregation; (ii) a spike of the demand in one part of the city increases the prices all over the city; (iii) subsidies are more efficient than taxes in fostering social mixing.

We represent the functioning of the housing market and study the relation between income segregation, income inequality and house prices by introducing a spatial Agent-Based Model (ABM). Differently from traditional models in urban economics, we explicitly specify the behavior of buyers and sellers and the price formation mechanism. Buyers who differ by income select among heterogeneous neighborhoods using a probabilistic model of residential choice; sellers employ an aspiration level heuristic to set their reservation offer price; prices are determined through a continuous double auction. We first provide an approximate analytical solution of the ABM, shedding light on the structure of the model and on the effect of the parameters. We then simulate the ABM and find that: (i) a more unequal income distribution lowers the prices globally, but implies stronger segregation; (ii) a spike of the demand in one part of the city increases the prices all over the city; (iii) subsidies are more efficient than taxes in fostering social mixing.

PhD Thesis

Endogenous fluctuations in game theory and macroeconomics. University of Oxford

At all scales, economies undergo substantial fluctuations instead of changing smoothly over time. There exist two alternative views about these fluctuations. According to the first view, fluctuations are caused by exogenous noise. Absent noise, economies would return to stable stationary states. The second view argues instead that such stationary states are unstable, and economies endogenously fluctuate following limit cycles or chaotic attractors. Endogenous fluctuations would occur even without noise. It is not yet clear which of these two interpretations most closely describes economic reality, but it has fundamental intellectual and policy implications. This thesis presents theoretical arguments in favor of the second view, in both micro- and macro-economic systems.

At all scales, economies undergo substantial fluctuations instead of changing smoothly over time. There exist two alternative views about these fluctuations. According to the first view, fluctuations are caused by exogenous noise. Absent noise, economies would return to stable stationary states. The second view argues instead that such stationary states are unstable, and economies endogenously fluctuate following limit cycles or chaotic attractors. Endogenous fluctuations would occur even without noise. It is not yet clear which of these two interpretations most closely describes economic reality, but it has fundamental intellectual and policy implications. This thesis presents theoretical arguments in favor of the second view, in both micro- and macro-economic systems.

In the first part, we study the smallest scale at which these two alternative views can be compared. This is a normal form game repeatedly played by two players who learn from their mistakes and form beliefs about their opponents’ future play. Under the exogenous view, players would converge to a Nash equilibrium, and strategic fluctuations would only be caused by behavioral noise. The endogenous view argues instead that strategic dynamics may fail to converge to equilibrium. Here, we completely characterize convergence in games with two players and two actions per player under a learning rule known as Experience-Weighted Attraction. We also introduce a theory that we call “best-reply structure” to approximately characterize convergence in games with two players and an arbitrary number of actions. Our results show that non-convergence and so endogenous fluctuations are more common in games than what might be thought.

The second part of this thesis studies the largest scale of economic fluctuations, namely business cycles in macroeconomic systems. The two views propose different mechanisms to explain correlation, or comovement, of business cycles across economic sectors and across countries. The first view argues that comovement is caused by the propagation of shocks exogenous to the economy, such as political decisions and natural catastrophes. According to the second view, comovement is instead at least partially caused by the synchronization of non-linear dynamics that describe the business cycle. Here, we introduce a demand-driven model of endogenous business cycles in which synchronization occurs through input-output linkages. We develop a theory that mathematically illustrates the interplay between synchronizing non-linear dynamics, shock propagation and network structure. While exogenous business cycle models have difficulty to generate a level of comovement that is as high as in the data, synchronization of endogenous business cycles generates much stronger comovement, potentially solving long-standing puzzles in macroeconomics.